Best Health Insurance Plans in India That Cover Pregnancy in 2026

A practical, research-backed guide to the best maternity health insurance plans in India in 2026 — covering waiting periods, delivery limits, newborn cover, and what to watch out for before you buy.

Best Health Insurance Plans in India That Cover Pregnancy in 2026

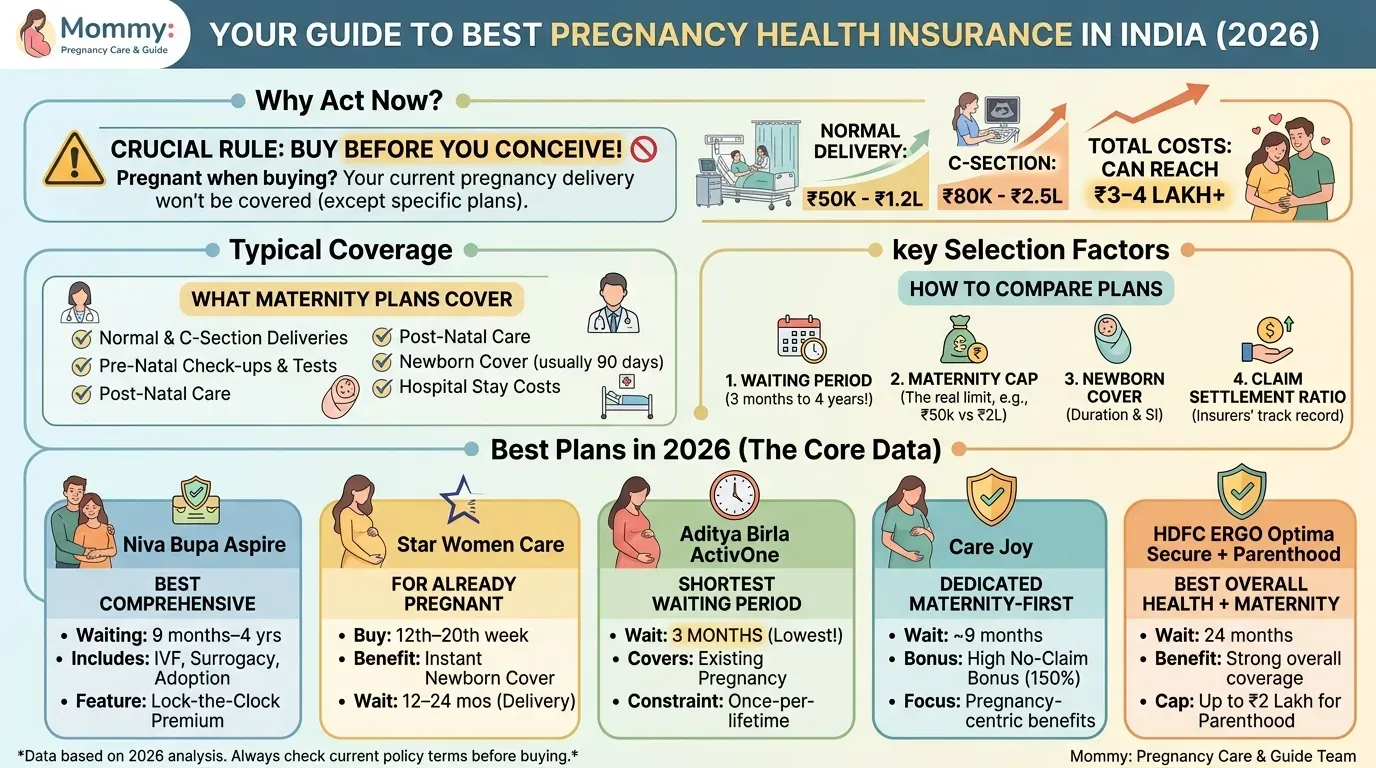

The cost of having a baby in India has risen significantly over the last decade. A normal delivery at a mid-range private hospital in a metro city typically costs between ₹50,000 and ₹1,20,000. A C-section — which accounts for roughly one in five deliveries nationally and closer to one in two at many urban private hospitals — often costs between ₹80,000 and ₹2,50,000 or more. Add antenatal consultations, ultrasounds, blood tests, and postnatal care, and the total cost of a pregnancy in a private setting can easily cross ₹3–4 lakh.

Health insurance with maternity coverage is one of the most practical steps a family planning a pregnancy can take — but it comes with a critical condition that most people discover too late: you cannot buy it once you are already pregnant and expect it to help with that pregnancy. Almost every maternity insurance policy in India has a waiting period — a period after buying the policy during which maternity claims cannot be made. That waiting period ranges from three months to four years depending on the plan.

This guide covers the best maternity health insurance plans available in India in 2026 — what each covers, how long the waiting period is, what the limitations are, and how to decide which one makes sense for where you are right now.

The Most Important Thing to Know Before Reading Further

Buy maternity insurance before you need it. This single piece of advice is more important than any comparison of specific plans.

Most standard health insurance plans do not include maternity coverage by default, and the benefits come with waiting periods and strict caps. All maternity insurance plans in India come with a waiting period — there is no maternity insurance without a waiting period currently available. Women should buy maternity health insurance as early as possible to finish serving the waiting period before they decide to start a family.

Many couples often wonder whether health insurance covers pregnancy if already pregnant. The answer is that many standard policies usually do not include maternity benefits if purchased after conception, as the insurance company considers it a pre-existing condition.

Plan ahead. Buy early. Then read this guide to figure out which plan to buy.

What Maternity Health Insurance Actually Covers

Before comparing plans, it helps to understand what the coverage actually includes — because the headline benefit (delivery expenses) is accompanied by sub-limits and caps that significantly affect how much you actually receive.

A comprehensive maternity health insurance policy in India typically covers:

- Normal delivery and C-section delivery expenses

- Pre-natal care expenses (doctor consultations, antenatal check-ups, blood tests, ultrasounds)

- Post-natal care expenses (follow-up consultations and medications after delivery)

- Hospitalisation costs during delivery (room rent, nursing, medicines during stay)

- Newborn care — coverage for the baby from birth, typically for 90 days

- In some plans: complications of pregnancy requiring hospitalisation

- In premium plans: IVF and assisted reproduction, surrogacy, in-utero fetal surgery

What it does not cover:

- Infertility treatments in most standard plans

- Pre-existing conditions affecting pregnancy

- Congenital diseases in some plans

- Cosmetic procedures

- Any amount above the maternity cap is out of pocket, even if your overall sum insured is much higher. Maternity cover can reduce the bill but the sub-limit is the binding constraint on what you actually receive.

The Five Best Maternity Health Insurance Plans in India in 2026

1. Niva Bupa Aspire — Best for Comprehensive Maternity Coverage With IVF

At a glance:

The maternity waiting period depends on the variant chosen: 4 years for Gold Plus, 2 years for Diamond Plus, and 9 months for Platinum and Titanium Plus plans.

Niva Bupa Aspire’s M-iracle benefit covers IVF, surrogacy, antenatal check-ups, delivery charges, adoption expenses, and more, with coverage that can accumulate up to 10 times the original sum insured.

Why it stands out:

Niva Bupa Aspire is arguably the most comprehensive maternity plan available in India in 2026. The M-iracle (maternity miracle) benefit goes significantly beyond what most plans offer — covering not just standard delivery but IVF, surrogacy, and adoption expenses within the same benefit structure. The Fast-Forward Benefit allows policyholders to access the full multi-year Base and Maternity Sum Insured from Day 1 of the policy term.

Niva Bupa provides access to a wide network of 10,400+ empanelled hospitals across the country. Cashless claims are processed within 30 minutes at network hospitals.

The Lock-the-Clock feature locks your premium at the age you first buy the policy — meaning if you buy at 25, you pay that age’s premium until you make a claim. For young buyers planning a family in the next few years, this is a significant long-term financial advantage.

Key details:

- Sum insured: ₹5 lakh to ₹1 crore

- Waiting period: 9 months (Platinum+/Titanium+ variants) to 4 years (Gold+)

- Newborn coverage: Covered from day 1 if maternity claim is paid

- Hospital network: 10,400+

- Covers: Normal delivery, C-section, IVF, surrogacy, adoption, antenatal care

Who it is best for: Young couples who want the most comprehensive maternity and fertility coverage, are buying well before planning a pregnancy, and want premium lock-in. The Platinum+ or Titanium+ variant with its 9-month waiting period is the most relevant for most families planning in 1–2 years.

Watch out for: Premiums are on the higher side. Recent customer feedback has highlighted rising service issues and increased complaints. Compare service quality reviews before committing.

2. Star Women Care Insurance — Best for Women Who Are Already Pregnant

At a glance:

Star Women Care Insurance Policy covers delivery, newborn expenses, antenatal care, and OPD consultations, with maternity benefits available after a 12–24 month waiting period. Assisted reproductive procedures (IVF, IUI, surrogacy, oocyte donor) carry a 3-year waiting period. Sum insured ranges from ₹5 lakh to ₹1 crore.

Why it stands out:

Star Women Care is uniquely positioned in one important respect: unlike most health insurance plans, pregnant women can buy this policy by submitting scan reports taken between their 12th and 20th week of pregnancy. This does not waive the waiting period for delivery expenses — the delivery itself will not be covered under the maternity benefit for that pregnancy — but it does mean a newborn baby is covered up to ₹2,50,000 from the date of delivery until 90 days without any extra premium.

For women who are already pregnant and seeking insurance, this is one of the few plans that will accept them at all, and the immediate newborn coverage is a meaningful benefit for the current pregnancy even if the delivery itself is not covered under maternity limits.

The plan is designed exclusively for women and covers a wide range of women-specific health concerns beyond maternity, including assisted reproduction and in-utero fetal surgery. A cashless hospital network of over 14,000 hospitals nationwide is available.

Key details:

- Sum insured: ₹5 lakh to ₹1 crore

- Waiting period: 12–24 months for delivery expenses; 3 years for IVF/assisted reproduction

- Newborn coverage: From birth for 90 days (immediate, subject to caps)

- Delivery coverage: Up to ₹50,000 for maximum 2 deliveries (at ₹10 lakh sum insured)

- Can be bought during pregnancy: Yes (12th–20th week with scan submission)

- Hospital network: 14,000+

Who it is best for: Women who are already pregnant and want immediate newborn coverage from birth for the current pregnancy. Also suitable for women who want a women-specific plan covering fertility treatments with a broad hospital network.

Watch out for: Extensive sub-limits — delivery coverage is capped and can fall short in metro hospitals, especially for C-sections. Star Health’s overall claims performance has been inconsistent and generally weaker than that of top insurers like HDFC Ergo and Aditya Birla. The delivery coverage cap of ₹50,000 at a ₹10 lakh sum insured is low for premium city hospitals where C-sections regularly cost ₹1.5–2.5 lakh.

3. Aditya Birla ActivOne Maternity Plan — Best for Shortest Waiting Period

At a glance:

The Aditya Birla ActivOne Maternity plan provides maternity coverage for existing pregnant women as well as women planning their pregnancy. It comes with a minimal waiting period of 3 months.

Why it stands out:

The Aditya Birla ActivOne Maternity Plan stands out as one of the few options that provide coverage to women who are already pregnant. It has one of the lowest waiting periods in the industry. Three months is the shortest waiting period of any maternity insurance plan in India — significantly below the industry standard of 9 months to 4 years.

Unlike most health insurance plans, the Aditya Birla ActivOne Maternity plan provides maternity coverage to women who are already pregnant as well as those who are planning a pregnancy. However, this coverage is available only once in the lifetime of the policy.

The plan also includes unlimited restoration of sum insured from day 1 (Super Reload benefit), a 5x renewal bonus, and no room rent capping — significant features for a comprehensive plan.

Key details:

- Waiting period: 3 months (lowest in India)

- Coverage: Normal delivery and C-section

- Can be bought if already pregnant: Yes

- Lifetime coverage: Once per policy lifetime

- Newborn coverage: Baby can be added after 90 days of birth

- Pre-hospitalisation: 90 days; post-hospitalisation: 180 days

- Available: 3-year policy tenure only

Who it is best for: Women who are already pregnant or planning to conceive soon and cannot serve a long waiting period. The 3-month waiting period is the most responsive option available in the market. The once-per-lifetime maternity coverage limitation is an important constraint — plan accordingly if you intend to have more than one child.

Watch out for: The coverage is available only once in the lifetime of the policy, and the policy must be for a 3-year tenure. Premium may be higher as a standalone maternity plan. Verify current delivery coverage caps before purchasing as these can change.

4. Care Joy Maternity Plan — Best for Dedicated Maternity-First Coverage

At a glance:

Care Joy is a dedicated maternity health insurance plan from Care Health Insurance, designed specifically for pregnancy and newborn care rather than as an add-on to a general health policy.

The Care Health Joy Health Insurance Plan covers pregnancy-related costs, postpartum costs, delivery costs, and problems. Sum insured choices ranging from ₹3 lakhs to ₹1 crore are available. The plan gives a no-claim bonus of up to 150% of the sum insured. The coverage pays for childcare treatments that call for less than a 24-hour hospital stay. The program offers a network of more than 11,000 hospitals in India with cashless healthcare options.

Why it stands out:

Care Joy is purpose-built for maternity — which means the coverage structure, sub-limits, and support features are designed around pregnancy rather than being a general health plan with maternity bolted on. Care Joy Maternity Insurance Plan covers pregnancy-related expenses including newborn baby care up to 90 days.

The pre- and post-hospitalisation coverage — 60 days before and 60 days after hospitalisation — covers the antenatal consultations and medications in a wider window than some competing plans. The no-claim bonus of up to 150% is among the highest available, meaningfully increasing the sum insured for families who don’t claim in a policy year.

Key details:

- Sum insured: ₹3 lakh to ₹1 crore

- Waiting period: Typically 9 months (verify current terms at purchase)

- Newborn coverage: Up to 90 days from birth

- Hospital network: 11,000+

- No-claim bonus: Up to 150% of sum insured

- Pre/post-hospitalisation: 60 days before, 60 days after

Who it is best for: Families who want a dedicated maternity-focused plan rather than a general health plan with maternity as one of many features. The high no-claim bonus is particularly valuable for the policy year in which no delivery claim is made.

Watch out for: As with all plans, verify the specific delivery expense caps at your sum insured level — the actual payout on a delivery claim is limited by the maternity sub-limit, not the overall sum insured.

5. HDFC ERGO Optima Secure with Parenthood Add-On — Best for Combining Maternity with Strong Overall Health Coverage

At a glance:

The HDFC ERGO Parenthood Add-on attaches to a base health policy and has a 24-month waiting period from the date it comes into force. It covers delivery and pre- and post-natal care.

Why it stands out:

HDFC ERGO’s approach to maternity coverage is different from the other plans on this list — rather than a standalone maternity plan or a maternity-first policy, it is a rider (add-on) attached to the Optima Secure base plan, which is one of the highest-rated comprehensive health insurance plans in India.

The advantage of this approach is that you get genuinely excellent overall health coverage — HDFC ERGO has one of the strongest claim settlement records and service reputations among Indian health insurers — with maternity benefits added on. The base Optima Secure plan offers comprehensive hospitalisation coverage, no room rent capping, restoration of sum insured, and a wide hospital network.

If you conceive during the waiting period but the delivery occurs after the waiting period has ended, the delivery will be covered. This is an important nuance — the delivery date, not the conception date, determines whether the claim is eligible.

Key details:

- Waiting period for maternity: 24 months

- Coverage: Normal delivery and C-section; pre- and post-natal care

- Parenthood add-on sum insured options: ₹50,000 / ₹1 lakh / ₹1.5 lakh / ₹2 lakh

- Hospital network: 10,000+

- Claim settlement: One of the strongest in India

Who it is best for: Families who want the best overall health insurance plan with maternity added on, and who are comfortable with a 24-month waiting period. If you are 1–2 years away from planning a pregnancy, this is the most balanced option for comprehensive health protection alongside maternity coverage.

Watch out for: The Parenthood add-on sum insured options (up to ₹2 lakh) may be insufficient for high-end private hospital C-section costs in metro cities. Plan for out-of-pocket costs above the add-on limit. The add-on can only be purchased at policy inception or renewal — not mid-term.

Side-by-Side Comparison

| Plan | Waiting Period | Delivery Coverage | Newborn Cover | IVF/ART | Buy While Pregnant | Hospital Network |

|---|---|---|---|---|---|---|

| Niva Bupa Aspire (Platinum+) | 9 months | Up to maternity SI | Day 1 (if maternity claimed) | Yes | No | 10,400+ |

| Star Women Care | 12–24 months | Up to ₹50,000 (at ₹10L SI) | 90 days from birth | Yes (3-yr wait) | Yes (12–20 wks) | 14,000+ |

| Aditya Birla ActivOne Maternity | 3 months | As per plan terms | After 90 days | No | Yes | 10,000+ |

| Care Joy | 9 months | Up to maternity SI | 90 days from birth | No | No | 11,000+ |

| HDFC ERGO + Parenthood Add-on | 24 months | Up to ₹2 lakh | Per base plan | No | No | 10,000+ |

What to Look For When Comparing Plans

Waiting period. This is the single most important factor. Most agent tasks don’t need your most powerful and expensive model. Sorry — wrong paste. Planning a baby soon? The waiting period is the make-or-break factor. A 9-month plan bought today means coverage by early next year. A 4-year plan is useful only if you have years to spare before planning.

Maternity sub-limits. A policy with ₹10 lakh sum insured does not pay ₹10 lakh for a delivery. The maternity benefit has its own cap — typically ₹25,000 to ₹2 lakh depending on the plan and the sum insured chosen. The cap is what you actually receive for the delivery. Check this number specifically, not just the headline sum insured.

Newborn coverage. How long is the baby covered, and for how much? Coverage for the first 90 days from birth, including NICU expenses if needed, is the standard to look for.

C-section parity. Confirm that C-section is covered at the same limit as normal delivery. Some older plans differentiated; current plans generally do not, but verify.

Claim settlement ratio. A plan with generous coverage that is difficult to actually claim is worse than a plan with moderate coverage that settles claims smoothly. Star Health’s overall claims performance has been inconsistent and generally weaker than top insurers. HDFC Ergo and Aditya Birla have stronger claims records. Check IRDAI annual reports for current claim settlement ratios before buying.

Hospital network. Confirm that hospitals in your city — and specifically the hospital where you plan to deliver — are on the insurer’s cashless network. A cashless claim at delivery removes the need to arrange large upfront payments and then seek reimbursement.

A Note on Employer Group Health Insurance

Many employed women in India receive group health insurance through their employer. Group policies often include maternity benefits with shorter or waived waiting periods — typically covering one to two deliveries. If you have employer health insurance, check its maternity terms before purchasing a separate maternity plan. You may already have meaningful coverage.

The limitation of employer group cover is portability — if you change jobs or leave employment, you lose the coverage. Some women may be eligible for maternity benefits through their employer’s group benefits plan; however, group insurance benefits are restricted and may not cover the total cost of pregnancy. An individual policy that you own independently of your employer provides security that group cover cannot.

The Bottom Line

Maternity cover can reduce the bill for normal delivery or C-section, especially in private hospitals where costs can spike suddenly. Even when the payout is capped, having a defined maternity benefit helps you plan deposits and avoid last-minute cash crunch.

The right plan depends on where you are in your timeline:

- Planning a pregnancy in the next 3 months: Aditya Birla ActivOne Maternity — the only plan with a 3-month waiting period

- Already pregnant: Star Women Care — the only plan that accepts applicants who are already expecting

- Planning in 9–18 months: Niva Bupa Aspire Platinum+ or Care Joy — 9-month waiting period

- Planning in 2+ years and want best overall health coverage: HDFC ERGO Optima Secure with Parenthood Add-on

- Want the most comprehensive maternity and fertility coverage: Niva Bupa Aspire with M-iracle benefit

Whatever you choose: buy it today, not when you find out you are pregnant. The waiting period is not negotiable, and the financial protection it provides — for deliveries that can cost ₹2–3 lakh at a private hospital — is among the most practical preparations you can make for becoming a parent.

This article is for general educational and informational purposes only and does not constitute financial or insurance advice. Policy terms, waiting periods, coverage limits, and premiums change regularly. Always read the current policy document and confirm coverage details with the insurer or a licensed insurance advisor before purchasing. Verify all figures on the insurer’s official website as details may have been updated after this article was written.